Introduction

When it comes to insurance in the United States, one key thing sets it apart from many other industries—it’s regulated primarily at the state level, not by the federal government. That means the rules that govern your car insurance in Texas might be very different from those in New York or California.

Understanding how insurance regulations work across states helps consumers make informed decisions, ensures fair treatment, and promotes transparency in the industry. In this article, we’ll explore how state insurance regulations work, what agencies oversee them, and why it matters to you as a policyholder.

Why Is Insurance Regulated by States?

The U.S. Constitution gives states the authority to regulate businesses that operate within their borders. In 1945, the McCarran-Ferguson Act confirmed that insurance regulation would remain under state control rather than federal jurisdiction.

This approach allows each state to tailor its insurance laws to its residents’ needs, economic conditions, and risk environments. For example, Florida’s insurance laws focus heavily on hurricane coverage, while California emphasizes wildfire protection and consumer privacy.

Who Regulates Insurance in Each State?

Every U.S. state and territory has its own Department of Insurance (DOI) or Insurance Commission, which oversees insurers, agents, and policyholders. These departments ensure companies comply with state laws, treat customers fairly, and remain financially stable.

Some of the key responsibilities of these state regulators include licensing insurance companies, approving rates and policy forms, monitoring financial health, and handling consumer complaints.

The National Association of Insurance Commissioners (NAIC) acts as a coordinating body for all 50 states, helping maintain consistency across different state regulations. It creates model laws and best practices that states can adopt or modify.

How Insurance Regulation Works in Practice?

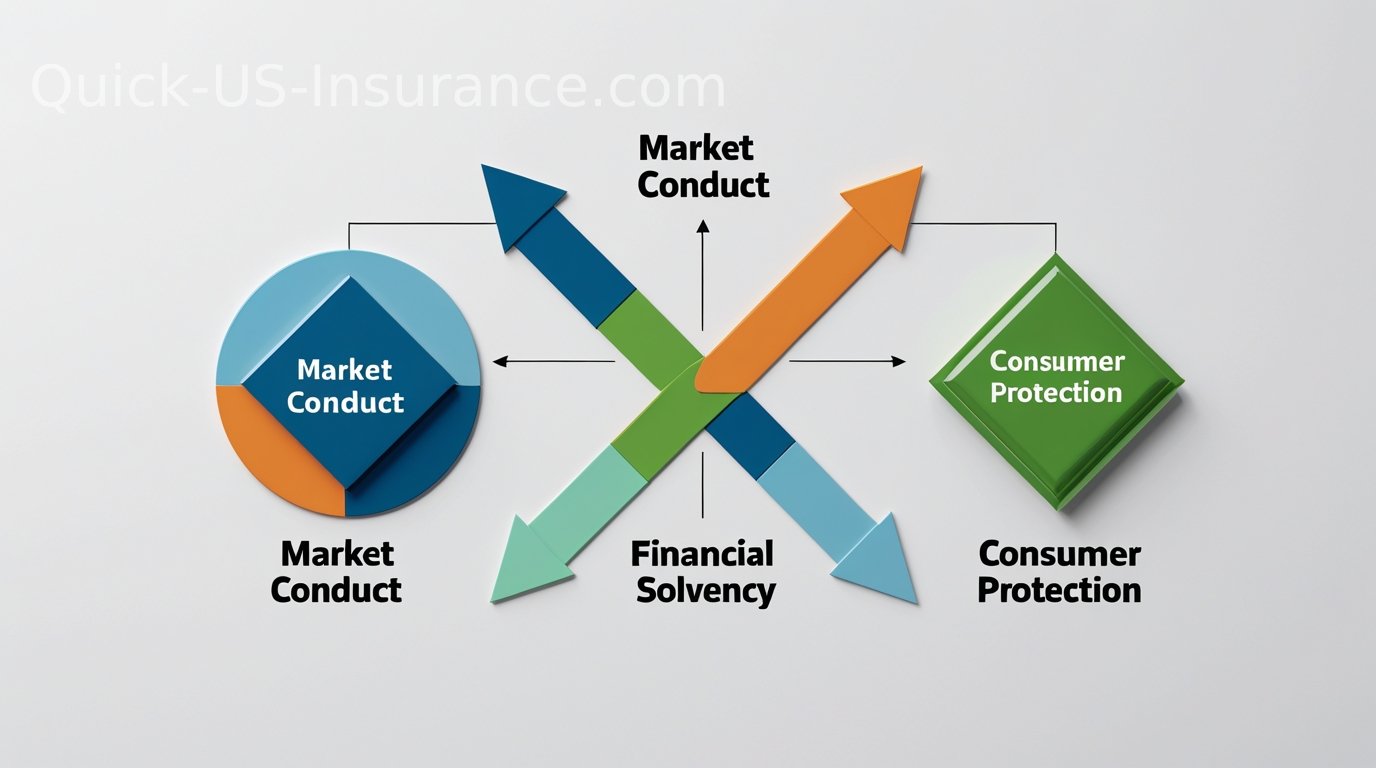

Insurance regulation in the U.S. covers three main areas: market conduct, financial solvency, and consumer protection.

- Market Conduct Regulation: Market conduct rules govern how insurance companies interact with customers—advertising, sales practices, claims handling, and renewals. States ensure fair play and prevent misleading marketing or delayed claims.

- Financial Solvency Regulation: States require insurers to prove they have enough reserves and assets to pay future claims. Regulators perform financial examinations on companies regularly to ensure policyholders’ protection.

- Consumer Protection: States provide complaint hotlines and advocate offices for consumers. These ensure transparency, protect against unfair practices, and provide resources for filing disputes.

How State Laws Affect Insurance Types?

- Auto Insurance: Each state sets its own minimum auto insurance requirements.

- California: $15,000 per person / $30,000 per accident for injury coverage.

- Texas: 30/60/25 liability rule.

- Florida: Requires no-fault Personal Injury Protection (PIP).

- Health Insurance: While federal laws like the ACA set nationwide standards, states control how insurers operate locally. Medicaid eligibility, network rules, and marketplace structures vary by state.

- Homeowners Insurance: Home insurance rules reflect local risks. Florida regulates hurricane coverage; California emphasizes wildfire policies. Some states offer government-backed coverage like FAIR Plans.

- Life Insurance: States require life insurers to disclose fees and maintain solvency reserves. Guaranty associations protect policyholders if an insurer fails.

How Are Rates Regulated?

Insurers must file rates for approval. Systems vary:

- Prior Approval: Rates must be pre-approved.

- File and Use: Companies can implement rates immediately after filing.

- Use and File: Rates go into effect before later filing.

How to Check Insurance Regulations in Your State?

You can visit your state’s Department of Insurance website for official laws and complaint forms. Examples:

- California: insurance.ca.gov

- Florida: myfloridacfo.com/division/consumers

- Texas: tdi.texas.gov

- New York: dfs.ny.gov

The Role of the NAIC

The NAIC coordinates state regulators and develops model laws like the Unfair Trade Practices Act. It also offers a Consumer Information Source (CIS) for checking insurer complaints and ratings.

Why State Insurance Regulation Is Good for Consumers?

Despite complexity, state-based regulation offers localized protection, transparency, and competition. Regulators are more accessible and responsive to consumers’ needs.

Conclusions

Insurance regulation in the U.S. may seem complex, but it’s designed to protect policyholders and promote fair markets. By understanding your state’s insurance laws and the role of its regulators, you’ll be better equipped to make confident decisions when buying coverage.